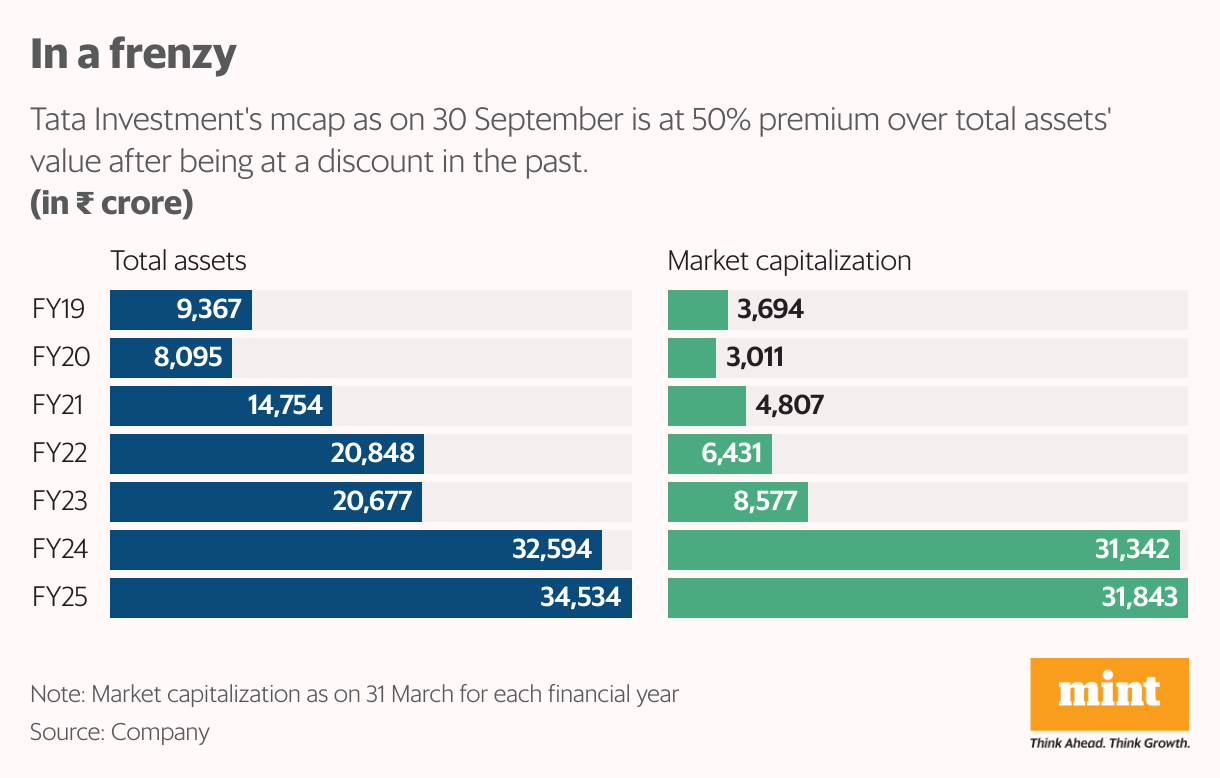

If Warren Buffett’s Berkshire Hathaway’s valuation is the benchmark, Tata Investment Corp. Ltd (TICL) looks overpriced. Berkshire’s market capitalization (mcap) of $1.08 trillion compared to its $1.15 trillion in assets gives it a mcap-to-assets ratio of ~1. By contrast, TICL’s ratio now stands at 1.5x after a 50% September rally lifted its mcap to nearly ₹54,000 crore.

Nearly 70% of TICL’s September gains came in just two sessions—on 23 September after a stock split (10-for-1) announcement, and on 30 September after Tata Capital’s IPO details were revealed. A closer look at both reasons suggests the stock’s reaction may be euphoric.

The stock split at TICL will improve liquidity but leaves fundamentals unchanged. TICL also owns about 80 million shares of Tata Capital. At a notional listing price of ₹500 (versus public issue price band of ₹310-326), this stake is valued at around ₹4,000 crore, compared to ₹2,300 crore already reflected in the books. Even so, the bump adds only about 5% to TICL’s total asset value of ₹34,000 crore as of 31 March.

TICL functions as a holding company, investing in both Tata and non-Tata firms with a long-term view. Its revenues primarily come from dividends, interest, and capital gains, with limited earnings from operations. For such companies, market value is best judged against the investment portfolio and growth prospects of investee firms, rather than price-to-earnings multiples, as earnings remain volatile depending on realized gains.

Quoted vs unquoted bets

Investments are usually divided into quoted and unquoted. TICL’s quoted investments may not bring any positive surprises.

Why? The market value of quoted equity shares at FY25-end was ₹29,597 crore against book value of ₹2,624 crore, leaving unrealized gains of nearly ₹27,000 crore—an amount that has not risen significantly so far in FY26.

Tata Consumer Products Ltd, Titan Co. Ltd, and Trent Ltd accounted for nearly 60% of the market value of the quoted investments. The sharp drop in Trent stock has offset the gains in shares of Tata Consumer and Titan.

Within unquoted investments, the Street may be excited about two big names: NSE and Tata Sons. Investments in NSE could be worth ₹1,000 crore. TICL has just 0.08% stake in Tata Sons that holds investments worth ₹13 trillion as on June-end with Tata Consultancy Services Ltd alone contributing 60%. That values TICL’s stake in Tata Sons at about ₹1,000 crore. Again, the numbers do not appear large vis-à-vis the overall portfolio size.

TICL has holdings in Tata Chemicals Ltd and Tata Motors Ltd, which in turn have holdings in Tata Sons, the listing of which is not decided yet. Here, Tata Chemicals appears to be a good bet given that the likely value of its stake in Tata Sons is more than its mcap.

Some optimists may argue that the growth potential of TICL’s investee companies could be higher than those of Berkshire. While that argument may be used to justify relative premium valuation of TICL, investors must approach the stock with caution.